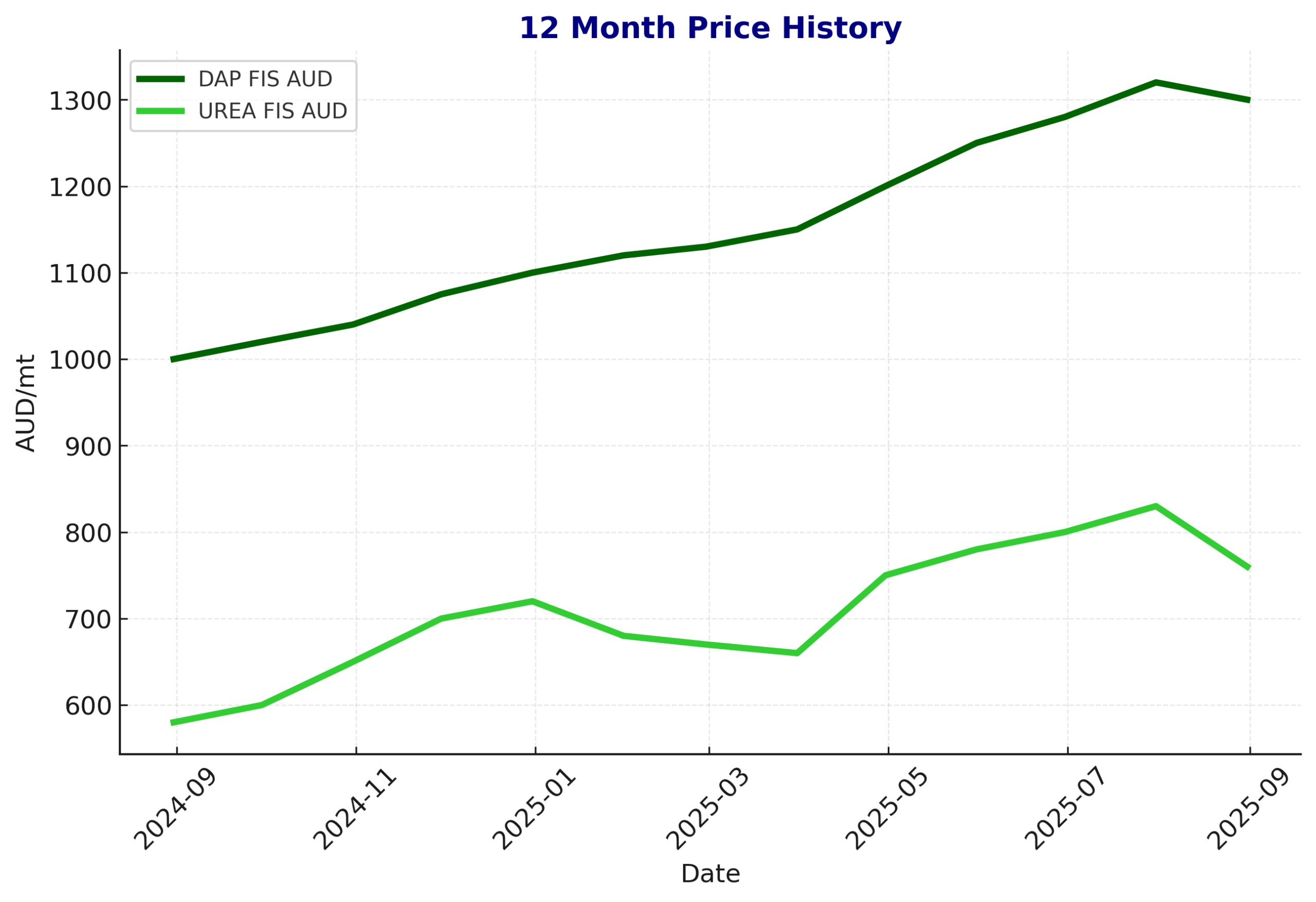

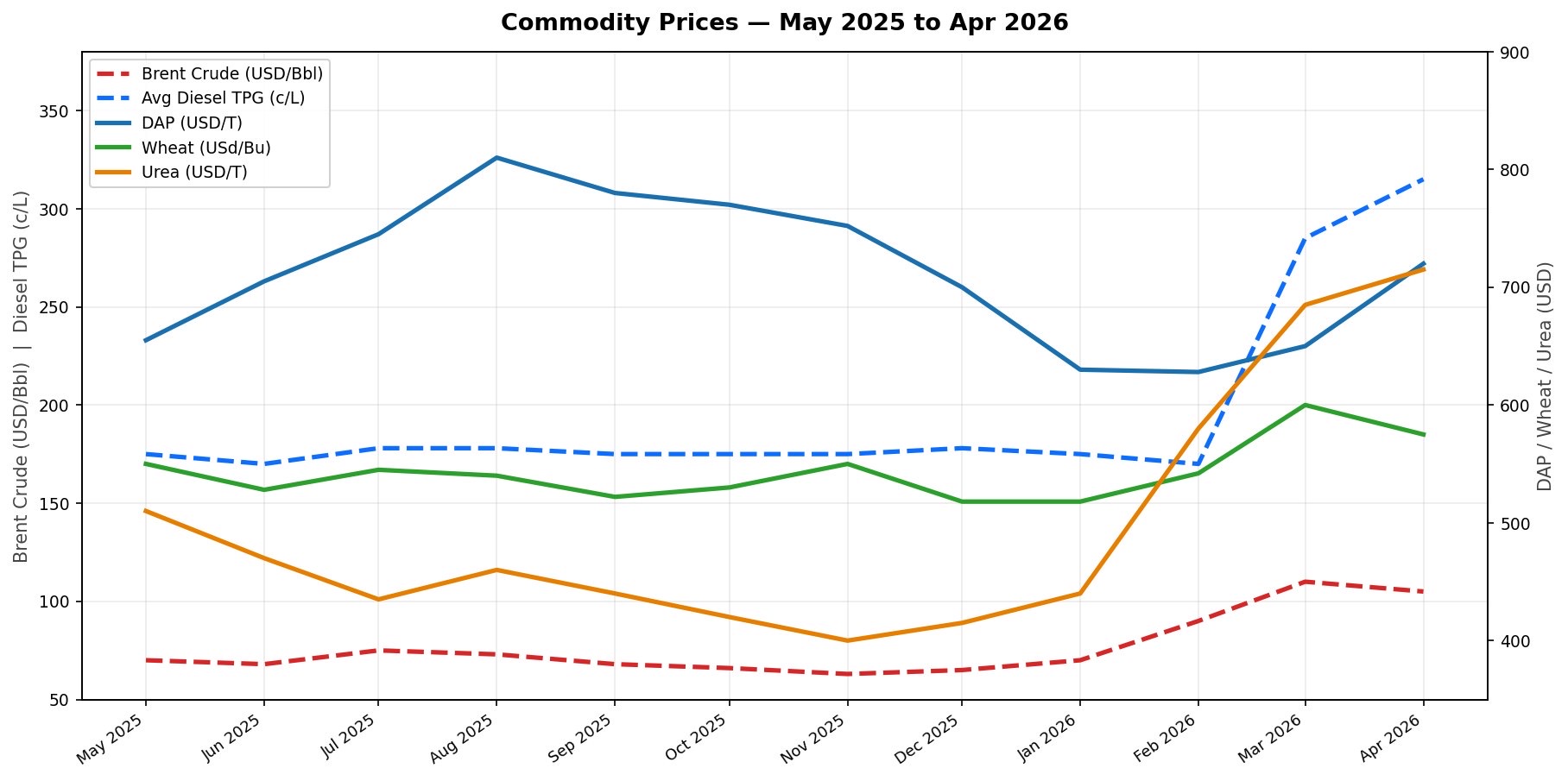

Fertiliser Pricing v Diesel Pricing

Still no joy with crop input costs as both fertiliser and diesel pricing remain high for the farmers. The below graph shows the affects of the conflict on the global commodities Urea, DAP, wheat, brent crude oil v's Brisbane's Diesel Terminal gate price.