GENERAL NEWS

The effects of the conflict are consuming the entire sector with the rapidly increasing input costs and supply chain issues posing challenges to the whole industry.

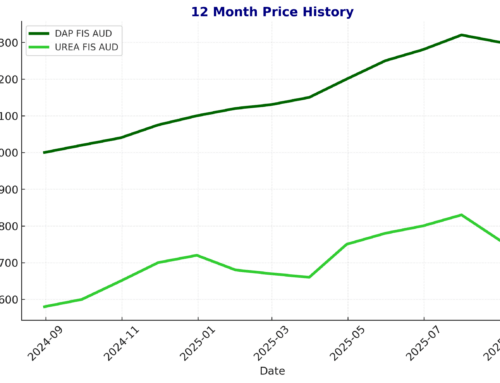

The urea price and diesel price have been on a similar trajectory over the last few weeks. Urea up ~75%, and Diesel has nearly doubled up from 166c/lt TGP to 311c/lt today. Long term supply for both products is still uncertain whilst there is no clear end to the conflict.

The diesel price has sent a massive shock throughout the freight industry, which has never seen a cost shock so large and so fast hit their sector. Most operators are bleeding money each week to keep the wheels turning and customers happy, hoping their diesel levy mechanism will catch up and be accepted by their customers.

There has been a lift in grain prices up to $35/t, but most of these gains are offset by the increase freight costs to port/customer. This makes for double trouble for those buying feed grain for their operations.

Growers are quickly approaching a point where the rising fertilizer prices, freight costs, and the potential for below-average rainfall, now make not planting winter crops (or a % of) a real option.

|