Most growing regions have received some rain over the last month, and some have seen flooding. However the majority of growing areas require a lot more moisture to give confidence for the winter season.

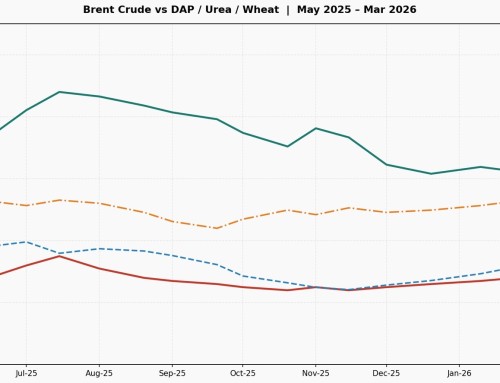

On the upside there has been some movement in most global commodity prices with products such as wheat, canola & cotton all on the rise.

Unfortunately these increases have not kept pace with inputs such as fertiliser and diesel over the last two weeks. The Iran conflict has rapidly sent shocks around the world and overnight we were surprised with a 20c jump in the diesel price to $2.20/lt terminal gate price (TGP).

The large input cost increases and supply chain disruptions will pose challenges to the whole industry over the next 3-6 months.

WEATHER

With what’s going on around the world, trying to predict the longterm forecasts for rainfall could be detrimental.

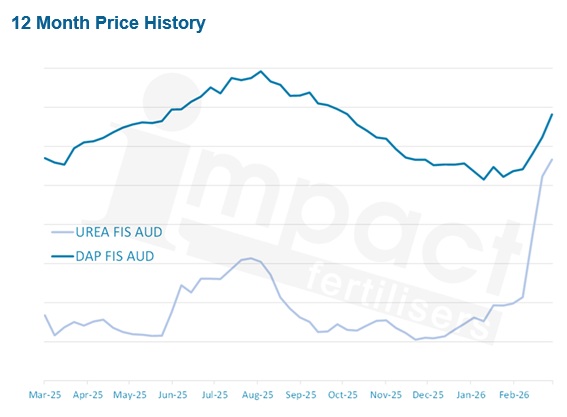

FERTILISER NEWS – 10th March 2026

Domestic fertiliser movements have moved quickly from the affects of the conflict in the middle east.

Urea prices have shot up around 45% from $830’s two weeks ago, with international FOB’s over $700 per tonne being reported. Supply will remain tight with limited export availability from key producers and producers being largely committed.

Pricing for AP’s have risen slower than urea, with increases of around 10% for the fortnight. Domestic supply for MAP and starter fertiliser is near non-existent for un-committed v

olumes.

The supply of all mainstream fertiliser products will remain tight for sometime.

Sulphur has been increasing in price from global demand, but the conflict will keep upward pressure on this commodity.

SPONSORSHIP

Pacific Fertiliser sponsors sporting clubs in regional areas and we are behind numerous Rugby clubs again this winter. If you think you have good proposition for us, let us know.