FERTILISER NEWS – 9th Sept 2025

Domestic fertiliser movements have slowed in recent weeks, due to the end of the top dressing window, high fertiliser prices and low commodity prices. Global production, overseas tenders and a brief Chinese export window are putting pressure on pricing.

Currently the short term outlook for urea and AP’s is soft to flat. However with China’s export window closing in mid October, upcoming tenders from India, Brazil and others, prices could find support close to current levels.

Urea prices are currently soft, but large summer crop planting may cause short-term nitrogen supply issues, so it is best to understand and lock in your requirements.

FERTILISER PRICING – 9th Sept 2025

Fertiliser prices over the last two weeks have remained fairly stable.

Urea – the price is soft. Domestically the price has been flat and contracting remains low.

Phosphates – AP’s the price remains soft to flat. Domestically the price has been flat and contracting remains low.

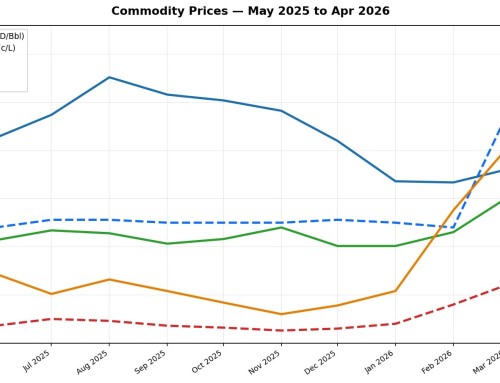

The current eastern fertiliser market is trading in the following ranges:

Urea late $800’s (not much getting contracted at the moment)

MAP/DAP low $1300’s

Starter Z – very tight supply – mid $1400’s

SOA low-mid $400’s

SSP low $500’s (limited supply)

MOP has been steadily increasing, in the $700’s

SOP mid-late $1200’s

Feel free to contact us for firm pricing and options. |